Are you confused by legal jargon and wish a lawyer could explain it? That’s exactly what we’ve done in this legal glossary series. This time, our experienced Chicago car accident lawyers explain the difference between duty to defend vs. duty to indemnify.

When you buy insurance, it’s important to understand two key terms—duty to defend and duty to indemnify. The duty to defend means it is your insurer’s obligation to provide a lawyer and pay legal costs if you’re sued over a covered incident. The duty to indemnify means your insurer pays any damages you owe if you’re found responsible.

Knowing these differences in policy coverage—along with your policy limits—helps you make informed insurance choices.

En este artículo

Understanding Duty to Defend and Duty to Indemnify

When you purchase an insurance policy, you enter into an insurance contract. This agreement gives both you and your insurance company specific rights and responsibilities. Two of the most important insurer’s duties are the duty to defend and the duty to indemnify. Understanding these concepts is essential when shopping for a liability insurance policy.

What Is the Duty to Defend?

The duty to defend is an insurance company’s legal obligation to provide you with legal representation in a potentially covered claim. If you are accused of negligence that leads to a lawsuit, your insurer may be required to hire and pay for a lawyer to defend you in court. This duty covers the legal fees associated with claims arising from accidents, injuries, or other events covered by your policy.

Ejemplo de deber de defensa

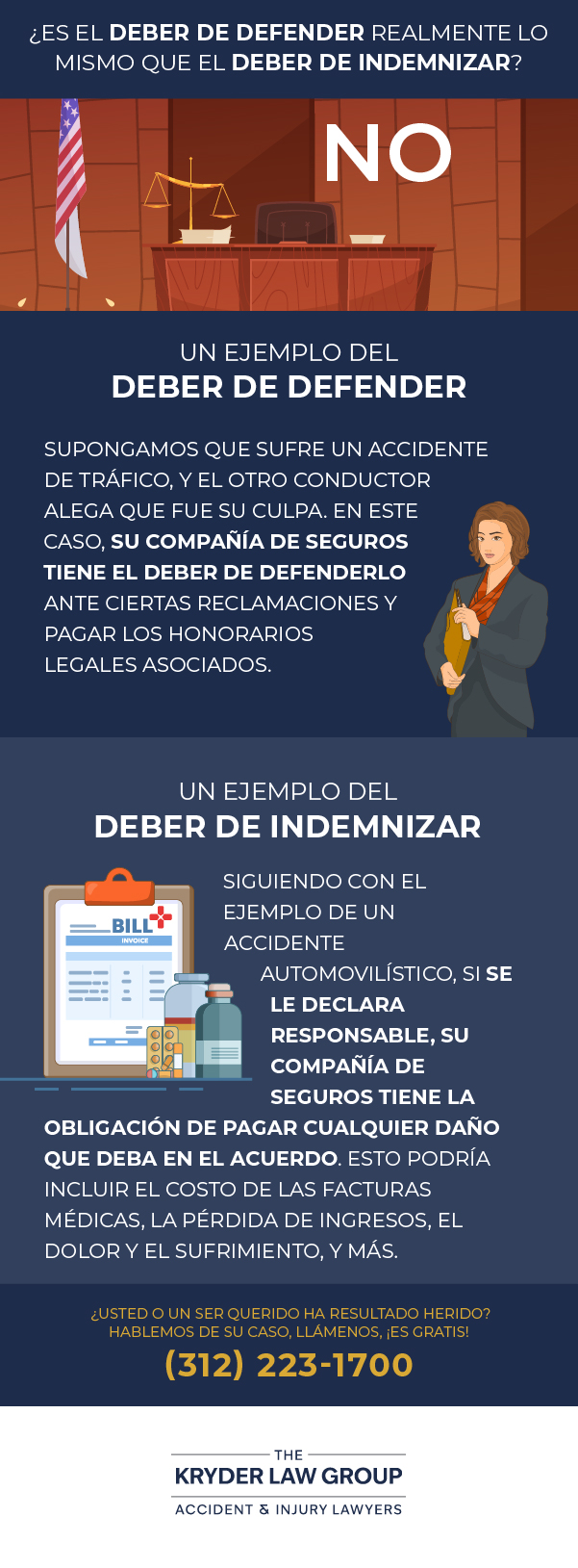

Imagine you are involved in a car accident, and the other driver sues you, claiming you were at fault. In this situation, your auto insurance company has a duty to defend you. They will handle the legal side of the underlying claim, paying for your own defense lawyers and associated defense costs.

What Is the Duty to Indemnify?

The duty to indemnify is about paying the money if you are found responsible for damages in the underlying suit. This is the insurance company’s obligation to cover the costs that a court orders you to pay as a result of a judgment against you. This can include compensation for the other party’s medical bills, lost wages, and pain and suffering.

An Example of a Duty to Indemnify

Let’s use the same car accident scenario. If the court finds you legally responsible for the crash, your insurance company’s duty to indemnify comes into play. They are required to pay the settlement or judgment amount, up to your policy limits. This payment covers the damages awarded to the injured party.

The Duty to Defend and Duty to Indemnify Are Different

Many people use the terms “duty to defend” and “duty to indemnify” interchangeably, but they are very different concepts.

The duty to defend involves providing legal representation to respond to allegations made against you. The duty to indemnify involves paying the money owed if you are found legally responsible in a lawsuit. In simple terms, one is about legal defense, and the other is about financial payment.

Can an Insurer Refuse to Defend or Indemnify?

Yes, an insurance company can refuse to defend or pay for a claim, but they need a valid reason. For example, they might deny coverage if the claim isn’t included in your policy or if there’s proof of fraud on your part. Sometimes, the insurer may ask a court through a declaratory judgment action to decide if they are legally obligated to defend or indemnify.

As a general rule, it’s crucial to read your policy language carefully to understand what is covered and what exclusions apply.

Have You Been Injured in an Accident?

If you have suffered an injury because of someone else’s negligence, navigating the legal and insurance process can be difficult. Our experienced attorneys can help you understand your rights and pursue the compensation you deserve. Call us today for a free consultation.

¿Le confunde la jerga jurídica? Deje que un abogado le explique la diferencia entre una cláusula de obligación de defensa y una cláusula de indemnización en una póliza de seguros.

(312) 223-1700

(312) 223-1700