If your insurance company says your bike is a total loss, you may want to use a total loss motorcycle value calculator to ensure you’re getting a fair offer. Insurers typically use the Actual Cash Value (ACV) method, which calculates the cost to replace your bike with a similar one, minus depreciation. You can reference this formula to estimate your compensation.

If you or a loved one has been injured in a motorcycle accident due to the recklessness of another person, our Chicago motorcycle accident lawyers can help. Call today for a free consultation.

In this Article

How to Use a Motorcycle Total Loss Value Calculator

What Is Full Market Value vs. Fair Market Value?

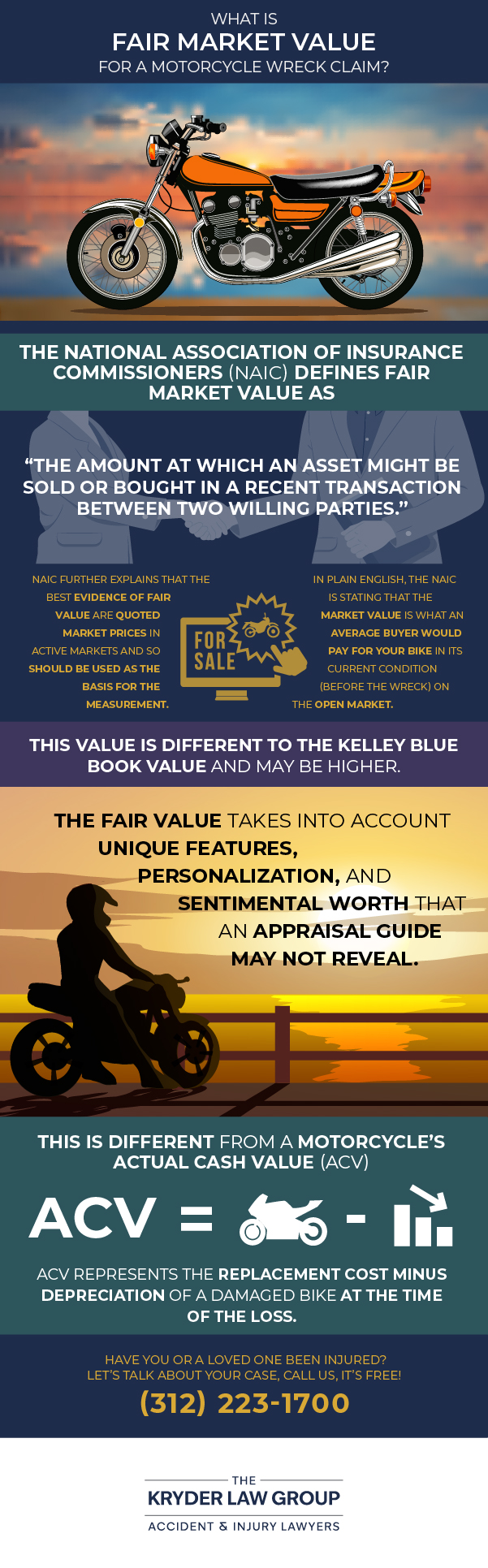

Full market value is the highest price your motorcycle could sell for on the open market. Fair Market Value (FMV) is the price both a buyer and seller would agree on if they had all the facts. FMV provides a more accurate and realistic estimate of your motorcycle’s worth.

What’s the Difference Between Actual Cash Value and Total Loss Value?

ACV is the market value of your motorcycle minus depreciation. Total Loss Value, however, is the payout you receive when your vehicle is declared a “total loss” after an accident.

Example Total Loss Motorcycle Value Calculation

If your motorcycle’s fair market value was $6,000 at the time of the wreck—but its scrap value is $2,000, and repairs cost $5,000—it’s considered “totaled.” This is because the combined scrap and repair costs ($7,000) exceed the fair market value.

How Is the Value of the Totaled Motorcycle Determined?

When an insurance company declares a total loss, they determine its value using data from sources like NADA or Kelley Blue Book. Adjusters also consider the selling price of similar models in your area.

Recent mods, upgrades, or improvements with receipts can increase the bike’s value for insurance purposes. The salvage cost is then deducted from the total value, as the insurance company usually takes ownership of the totaled bike.

How Much Is an Insurance Company Required to Pay Out for a Totaled Motorcycle?

Insurance companies’ payout amounts for totaled motorcycles are regulated by state insurance departments. The Illinois Department of Insurance oversees these operations. They ensure that insurance companies follow the Actual Cash Value method for calculating total loss payments.

What Is the Cutoff Value for Repair?

The cutoff value for repair is the damage cost threshold set by insurers to determine if a vehicle is a total loss. For example, if repair costs exceed 70% of the vehicle’s pre-accident value, it may be considered totaled.

How Do I Know If I Am Being Offered a Fair Settlement?

To see if your property damage settlement is fair, compare the insurer’s valuation to your motorcycle’s Fair Market Value. For example, if similar bikes in your area sell for $8,000, but your offer is $6,000, it may be worth negotiating.

Can the Repair Shop Install Used Aftermarket Parts to Repair My Motorcycle?

Yes, repair shops can use compatible, good-condition used parts to fix your motorcycle.

Can I Negotiate the Total Loss Value of My Motorcycle?

If you disagree with your motorcycle’s total loss valuation, you can challenge it by providing evidence like upgrade receipts or select examples of higher-priced listings. This could encourage the insurance company to adjust their offer.

Who Pays the Taxes and Transfer Fees for My New Motorcycle?

Insurance may cover taxes and transfer fees for a totaled motorcycle, but this varies by policy. Check your policy or ask your insurer for details.

What If I Owe More Than My Totaled Motorcycle Is Worth?

Being “upside-down” on your motorcycle loan means you owe more than the bike’s value. While it’s a tricky situation, options like gap insurance or lender negotiation can help.

What Do I Do If I Was Injured in a Bike Wreck?

If you have been injured in a bike wreck, some steps to take afterward would be to:

Seek immediate medical attention.

Inform your insurance company to initiate claim procedures.

Consult with a personal injury attorney to protect your rights.

Maintain a record of all medical documents and expense receipts.

What Factors Affect the Value of My Motorcycle?

The repair cost or replacement cost of your motorcycle can be influenced by:

Age and mileage: motorcycles depreciate over time; model year and mileage can significantly impact their value.

Condition: the overall condition of your motorcycle, including mechanical and cosmetic aspects like scratches, dents, or mechanical issues, can decrease the value.

Brand and model: certain motorcycle brands and models have higher resale values.

Modifications: custom modifications can affect your motorcycle’s value both positively and negatively; performance upgrades often enhance value, while unique paint jobs may lower it.

Market demand: the value of your motorcycle model in the used market is influenced by its demand; higher demand typically leads to a higher value.

Maintenance records: well-maintained motorcycles with full service records often command higher prices.

How to File a Total Loss Insurance Claim for Motorcycles

Some steps include:

Report the incident to your insurance provider to start the claim process.

Take photos of the damage and note key details to support your claim.

Collect all necessary motorcycle paperwork, including details, receipts, and service records.

Get a professional mechanic to assess the damage to your motorcycle.

Negotiate with your insurance company to determine a fair settlement value.

Confirm and accept the settlement offer.

What Happens to My Motorcycle After a Total Loss Settlement?

In Illinois, the insurance company usually takes ownership of salvage title to the damaged motorcycle and sells it to a salvage yard for scrap value.

If I Keep the Salvage, Can I Still Ride My Motorcycle?

In Illinois, you can keep a salvage motorcycle if it passes inspection, gets a “rebuilt” title, and is deemed roadworthy.

How Long Does the Total Loss Claim Process in Illinois Take?

The total loss claim process usually takes several weeks, depending on case complexity, information exchange speed, and settlement negotiations. Prompt communication with your insurer can help speed up the process.

If you or a loved one has been injured in a motorcycle accident due to the recklessness of another person, our Chicago motorcycle accident lawyers can help.

Do I have a case?

Phone Number

Fax

Address

134 North LaSalle St., Suite 1515 Chicago, IL 60602 Get Directions

Settlements & Verdicts

$7.5M

$7.5 Million Recovered for a Construction Worker Injured on Site

$3M

$3 Million Recovered for the Family of a Person Struck by a Garbage Truck

$2.2M

$2.2 Million Recovered for a Salesperson Injured in an Automobile Collision

$2M

$2 Million Recovered for a Person Struck by a Speeding Vehicle While Waiting for the CTA Bus

$1.4M

$1.4 Million Recovered for a Computer Programmer Injured in a Slip and Fall

$1M

$1 Million Recovery in just 90 Days for the Family of a Man Killed While Helping a Stranded Motorist

(312) 223-1700

(312) 223-1700